Fund Update — Q1 2023

Previous quarterly update:

Fund Update Q4 2022

Q1 2023 Venture Investments

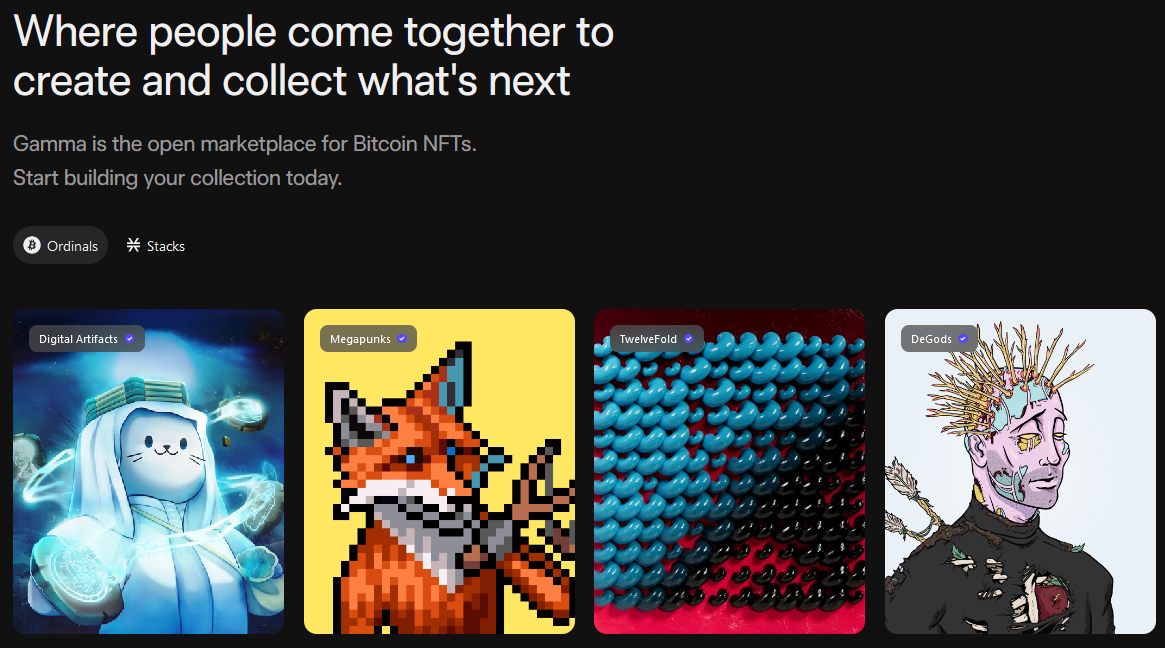

Gamma (Seed, New)

We were thrilled to connect with Jamil and Nick, the Founders at Gamma. Long before the recent take-off of Bitcoin NFTs and digital assets, they've had a high conviction bet building in this area.

Gamma is the #1 marketplace for Stacks and BNS (Bitcoin Name System) NFTs. Stacks is one of our earliest investments from 2017 that we've held over the years, that has outperformed the market recently due to increased demand in Bitcoin blockspace due to Ordinals and Inscriptions.

Their thesis is now coming to fruition and they've built the best UX and community for Bitcoin NFTs. We also believe that Bitcoin is the most pristine, valuable blockspace for NFTs and stands out from other chains in terms of true asset ownership, storage, and permanence, given the game theory of Proof of Work. The use-cases around Inscriptions and being able to store data on the Bitcoin blockchain is just beginning.

Gamma is balancing UX, sovereignty, and self-custody of Bitcoin digital assets in a way that both maximizes security and brings usability to the masses. They are also focused on APIs that will help expand these features to new apps.

Check out their recent announcement post here!

Karate Combat (Seed, New)

Karate Combat will be the first sports league fully transferred into a DAO ownership model. They bring on premier fighters for their unique striking-focused fights that are hosted as live events, streamed for free on the web, and sometimes pre-recorded events in their green screen sound stage, which offers a unique video game-like, digital aesthetic for viewers.

This deal stood out to us for a number of reasons but primarily around their focus on usability and abstraction for the average, non-crypto viewer and their unique approach on 'betting'. Users of the upcoming Karate Combat app can bet on the winners of fights. After signing a smart contract, correct bets will automatically yield KARATE tokens. Wrong bets do not have any downside, so this is not sports betting in any traditional sense, it is an incentivization and rewards program.

Karate Combat already has huge traction, viewership and substantial revenues, which is rare in crypto. They are now making a high conviction bet on crypto being a core part of fan engagement in the future and this stood out to us.

Check them out more here!

Market Moves and Outlook

Since our last update, there have been major events in the market in the banking sector and uncertainty around where the economy is headed from here. We've continued to take a conservative approach in re-allocating capital into venture, public equities, and crypto as we navigate risk and define where we are in the cycle.

In Q4 last year, we wrote about potential contagion events in traditional markets following the crypto market turmoil of FTX, Celsius, etc. Our thesis was that the same market behavior and psychology that played out in an accelerated fashion in crypto was likely to play out in traditional markets in the banking and/or technology sectors. Since writing that piece, multiple banks (Silvergate, SVB, Signature, First Republic, Credit Suisse) have experienced failures to different extents and reasons, which has opened up questions of more bank runs and a broader credit crunch. It's possible the worst of this is over, but we believe there's likely more to come here in 2023, particularly in regional banks.

As a result of depositors being assured by governments that they will be protected, many are now calling for increased inflation, with some even predicting hyperinflation. We believe this to be misguided. While inflation may be stickier and take longer to decrease than expected due to energy prices going up again or lagged shelter data, it seems over the next year+, more disinflationary forces are here with bank runs, credit crunch, overall defensiveness, and potential recession on the horizon. The impact of interest rates being 5% and US inflation being at ~6% (with EU/UK much higher and generally lagging US data) will begin kicking in more now, as we generally see when real rates start to approach inflation. Real-time data on Truflation shows US CPI around 4% and while this will ebb and flow, the overall downtrend is more likely to stay its course. Once again, there's a possibility of a stickier CPI print in the middle of this and the market will certainly trade that negatively if that happens.

The current Fed activity is not equivalent by any means to 'helicopter money' or what we saw during COVID stimulus or Biden's 'infrastructure' bills that all overheated the economy. The mechanisms being used by the Fed will play out differently in the market, despite some people falsely comparing this phase to QE. We don't deny that monetary policy will eventually shift again and that MMT-esque policies aren't on the horizon once things 'reset' but we are not in the same economic environment as the 'easy money' period at all, as these are mostly defensive moves in reality. If additional bank runs occur, similar liquidity and loan facilities may be used which could have second order effects on increasing asset prices over time, but likely not on consumer inflation (outside of external forces in the energy market and OPEC+).

It's important to note, we have many criticisms of the Fed and aspects of the current system (i.e. the rapidly increasing nature of a control-economy versus a free market) but we are also realists, particularly when comparing the system to the rest of the world. As much as we love crypto, it is not a replacement economic system for the current one. It's not even close to being ready for that. We also don't believe crypto would perform well in another inflation scenario and is still seen as a risk / tech asset. If hyperinflation were to play out, that wouldn't be good for crypto. Crypto is a parallel economy that benefits from broader dollarization, while aspects of the existing system can certainly be improved by implementing crypto and ledger technology. In short, we are not "burn it all down" types and believe US hegemony is still better than any alternative. Being a visionary requires pragmatism and iteration, otherwise effective solutions will never come to fruition. We've written about populism a lot, both the good change and bad effects that can come from it. Seeing this kind of blind deconstructionist populism is not productive.

As of writing this, markets have actually had a nice bounce after the chaos at SVB et al was quelled (for now). The reason tech and growth stocks have likely run up in the last 2-3 weeks is the beginning of pricing in interest rates topping out and continued cooling CPI expectations. Moving into late 2023 / early 2024, rate cuts may also be in the cards. A disinflationary outcome for the remainder of the year is directionally bullish for risk assets, even if more choppy waters are ahead. The market also may be over-shooting how quickly this happens and may not be acting rationally, so we still expect to see chop. We may start seeing stronger recession signs where valuations and multiples take a hit, which could hurt risk assets again. Earnings still haven't fully cooled, so we expect some level of contraction there.

As mentioned in previous updates since Q3 of last year, we started buying Bitcoin at various levels and more substantially when it dropped below $20,000 and will continue focusing there, as we believe BTC dominance is likely to keep rising as liquidity comes back into crypto and regulation concerns increase. With a shift in monetary policy likely to begin some time in 2024, we also think Bitcoin will continue being the fastest horse and best vehicle to capture that upside. The demand for Bitcoin blockspace is also going up because of NFT usage and new use-cases, which is good for the network in our view.

Calls for the 'collapse of the US dollar' are perhaps the most irritating aspect of the current cycle, particularly with some in crypto predicting that would somehow be a positive for price. We are mid/long term bullish on crypto for much different reasons, not "dollar collapse". There are broader geopolitical factors going into this psyop, which we won't fully get into here. China and others will continue their political and symbolic moves to undermine the US dollar, but people are underestimating the dollar's network effect in our view. This negative sentiment on the USD could certainly create some issues in the near term, but similar calls for this have happened frequently in the past. It's also not a coincidence this narrative is being pushed in a down market, which is seen as an opportunity to reset the stage under a new standard. It's true the US dollar can and will go through these bigger issues one day, but crying wolf on that outcome being imminent is mostly engagement farming at this point (as is most modern day hysteria).

While transactions settled in CNY may increase a few percentage points over the coming years, we still think the world will fall back on the USD as a reserve currency for the foreseeable future. And that's not a bad thing. Anyone cheering on the USD collapsing should also realize the ramifications of that outcome. Power abhors a vacuum and despite all the US's flaws, you have to ask yourself what an alternative hegemony looks like and if you want to live in that world.

Bottom line is, we are still optimistic on US innovation and entrepreneurship being a jet fuel. Things will likely get worse before they get better, but will also appear worse than they really are as negative sentiment peaks (which is usually the best time to invest). There is massive innovation on the way in AI and biotech on the way. The quality of US technology, entrepreneurs, funding environment, financial reporting, transparency, etc., and how we export these things still matters in the long run and these things are not slowing down any time soon. Shorting America is still a very foolish endeavor.

This Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation, endorsement, or offer by Visary Capital or any third party service provider to buy or sell any securities or other financial instruments in this or in in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.